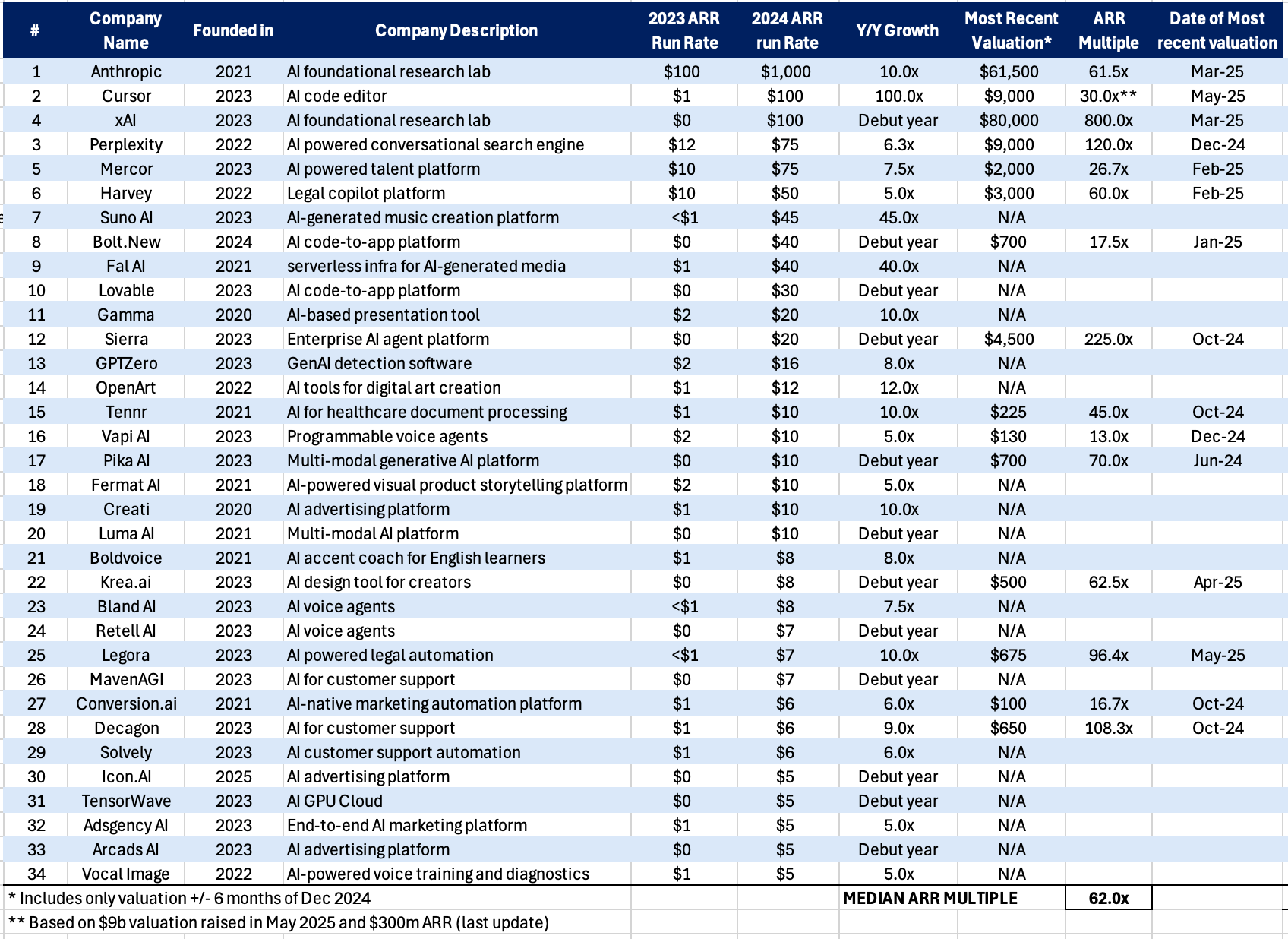

See below for a list of “555” AI startups — companies with >$5M in revenue, growing at least 5x y/y, and formed within past 5 years. 📈

The median revenue multiple for this group is ~60x trailing ARR — nearly 10x higher than the public SaaS average (~6x). That sounds rich… but:

➡️ The median growth here is 9x y/y – that’s fast! If a company “only” triples next year, the forward multiple drops to ~20x. Double again the year after, and it starts to converge with public SaaS valuations. It’s much easier to “grow into” a high multiple when your revenue is compounding fast.

➡️ Public SaaS companies grow only ~30% annually. The older ones are starting to trade off EBITDA instead of revenue.

In fact, research shows that forward ARR growth drives 60–70% of valuation in software. This percentage is even higher for early-stage growth companies (when I was a software investment banker, some of our R² were as high as 0.8-0.9)

So what does this mean for AI companies?

1️⃣ Growth is still king — it’s hands down the most dominant driver of valuation.

2️⃣ The super-fast growers (which I define as 20x+ y/y) aren’t in NLP: Cursor (code), Suno (music), fal (multimodal). Don’t be afraid to build beyond language.

3️⃣ Many of the companies in this list are building in prosumer/SMB markets. You don’t necessarily have to be building for enterprises. But for these companies, retention may carry a higher proportional weight.

4️⃣ Bottoms-up PLG motion is something many AI companies are leveraging. It’s very difficult to achieve >5x growth when relying solely on traditional top-down sales.

5️⃣ Only two companies in this list are training their own foundation models. Most companies are app-layer companies using foundation models as a substrate. Workflow + UI > model specificity. Don't build the engine, build the car.

6️⃣ Many companies are already cash-flow positive. With token costs declining, this may get even better. This is a big shift from past SaaS burn dynamics.

7️⃣ Founders face a classic tradeoff here then: Do you continue to grow profitably and minimize dilution? Or do you raise and try to accelerate market share capture? In my opinion, this decision is different for everyone but comes down to a few criteria: (1) how competitive is the market? (2) what’s the relative growth/dilution trade-off? (3) what’s the ROI on the incremental capital

In summary...

If there is one major difference between the AI era and the dot-com era, it's that the growth isn’t about “eyeballs” or “page views" this time — it’s real revenue!

What’s even more impressive — many of these companies have <30 employees. AI-native leverage is happening.

The pace is dizzying. The opportunity is real. And the next decade of software is being written right now.

The next FANGs are already here — just wearing different logos.

"The next FANGs are already here — just wearing different logos. " let's watch this space... Maybe some of the same logos