The dichotomy of fundraising and revenue in AI

The dichotomy of fundraising and revenue in AI

November 2023

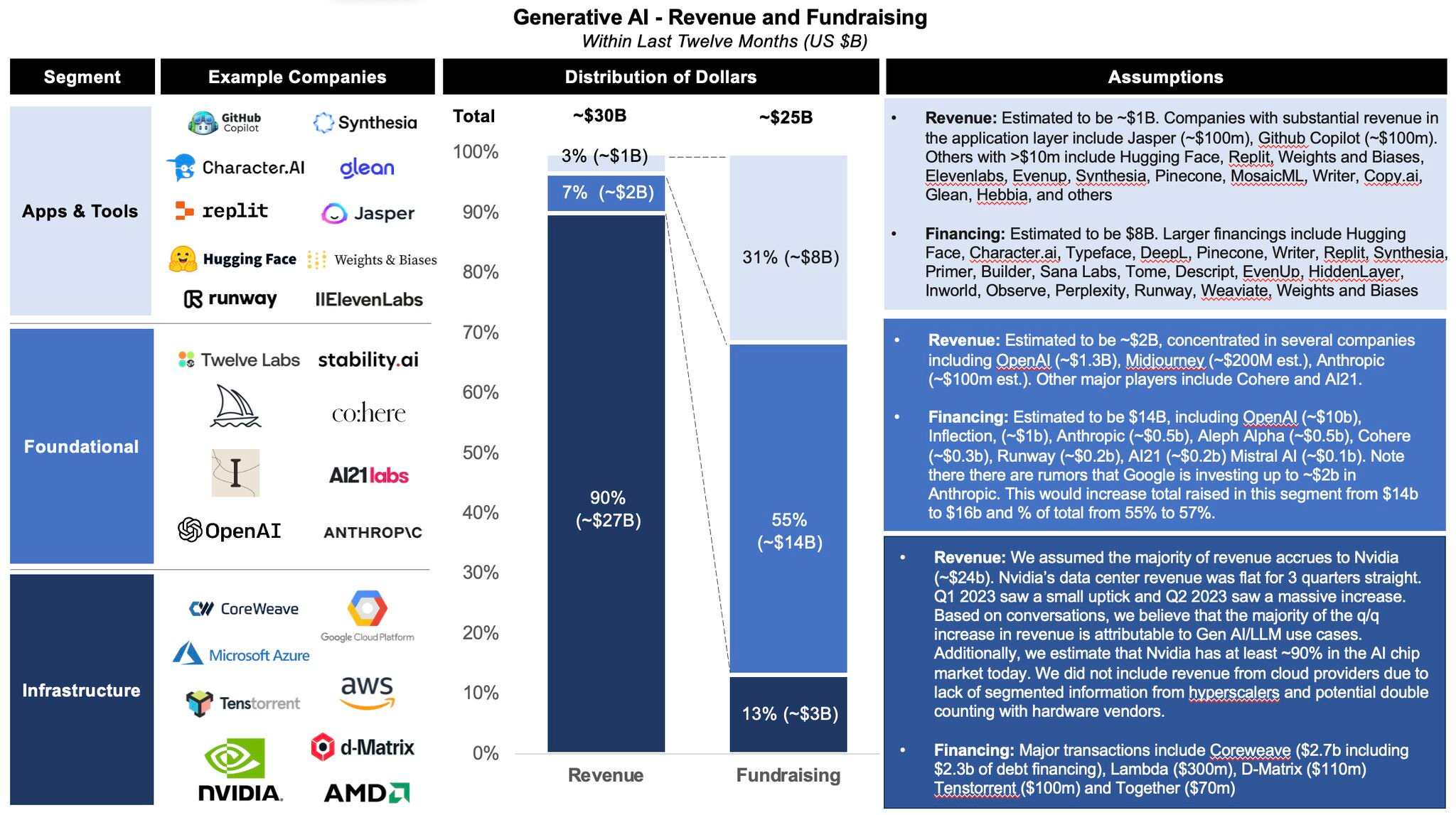

Check out this graph showing the distribution of revenue/fundraising dollars in generative AI. It looks deceptively simple but took me a few weeks of hard research to put together.

The TLDR: The vast majority of revenue in generative AI right now is being captured by infrastructure companies despite receiving only 13% of VC capital. By the same token, most of the fundraising is accruing to model and application companies even though they only account for 10% of the revenue.

Some questions to think about:

1️⃣ Why does this dichotomy exist in the first place?

The main reason is because it’s very early stages for Gen AI. Similar patterns existed throughout history where development and monetization in the infrastructure segment preceded the application segment. For example, internet infrastructure came first before internet applications such as search and ecommerce.

2️⃣ Will this pattern change anytime soon?

I would expect the current revenue distribution to maintain its current patterns in the short term. Although we might observe some growth in the model and application/tooling segment owing to a smaller starting base, it’s unlikely to catch up with the infrastructure segment. Nvidia’s data center revenue alone is expected to double to $40B next year. Moreover, as long as Nvidia continues to maintain a monopoly, prices for infra/chips will remain high. Lastly, much of the current compute we have today is allocated to the training side - we have yet to witness significant buildouts on the inference side yet. For all these reasons, I expect infrastructure to still be the predominant revenue engine for the foreseeable future.

3️⃣ What will the end state look like?

Over the long term, I would anticipate the TAM for the application and modeling stack to be 2-4x bigger than the infrastructure stack. If we look at more mature industries such as SaaS, gross margins are typically around 70-90%, with the majority of COGs going to cloud hosting costs. One can argue a similar margin profile will need to exist amongst native Generative AI businesses.

4️⃣ What will happen to fundraising?

Considering that up to 80% of the amount raised for foundational model companies goes to compute, I expect that fundraising for models will scale in proportion with infrastructure revenues. However, the application/tooling segment may be more volatile depending on if companies are able to grow into their valuations. This is dependent on how fast enterprises adopt generative AI solutions, which has been nascent so far.

In short, it appears that the only benefactor of generative AI in the past 12 months has been Nvidia. While this won’t last forever, substantial shifts will take time to materialize.